101 Emerging Effects of Digital Transformation in Banking- How It Benefits Banks and Customers in 2024

101 Emerging Effects of Digital Transformation in Banking- How It Benefits Banks and Customers in 2024

Introduction

Digital transformation in banking has significantly evolved, with 2024 witnessing a paradigm shift in how financial institutions operate and interact with customers. Powered by technologies such as AI, blockchain, cloud computing, and data analytics, the banking sector is redefining efficiency, security, and personalization. These changes benefit banks and customers, creating a win-win ecosystem.

Overview

Digital transformation in banking integrates cutting-edge technologies to automate processes, enhance customer experience, and innovate financial services. From open banking to hyper-personalized services, the industry is leveraging digital tools to address evolving market demands and customer expectations.

Importance

- Customer Experience: Personalized and convenient banking services are driving customer satisfaction.

- Operational Efficiency: Automation and digital tools streamline banking processes.

- Security and Compliance: Advanced technologies mitigate risks and ensure regulatory compliance.

- Innovation: Digital transformation enables banks to develop new financial products and services.

101 Emerging Effects of Digital Transformation in Banking

A. Enhanced Customer Experience

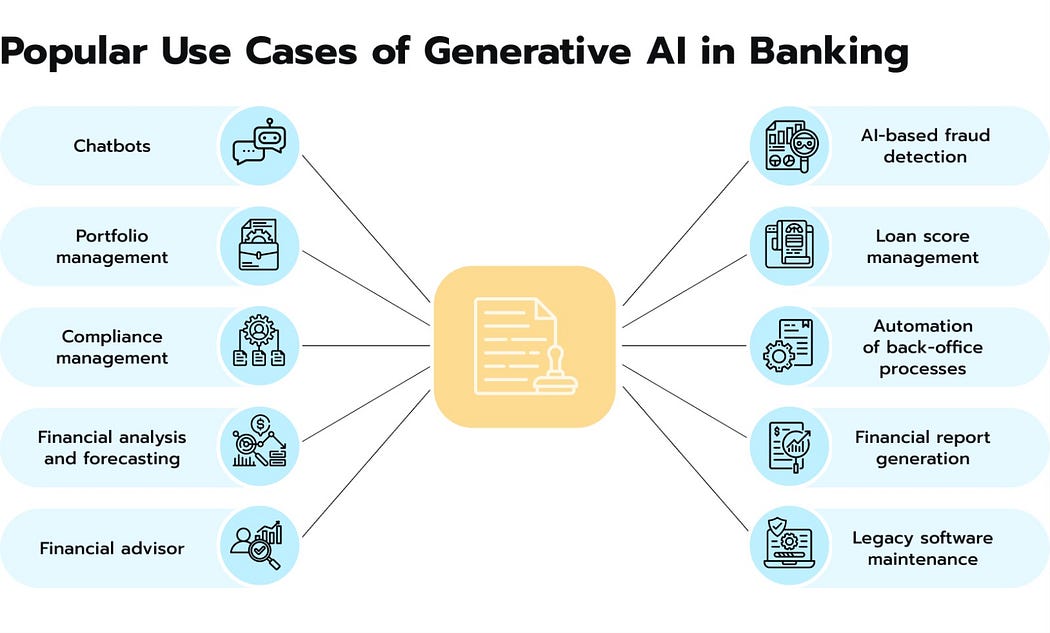

- 24/7 Banking Services: AI-powered chatbots and apps provide round-the-clock assistance.

- Personalized Recommendations: Data-driven insights for customized financial advice.

- Seamless Onboarding: Digital KYC for faster account creation.

- Intuitive User Interfaces: Simplified mobile and web platforms.

- Voice Banking: Interacting with banking services via voice commands.

B. Operational Efficiency

- Automated Workflows: Robotic process automation (RPA) for repetitive tasks.

- Real-Time Transactions: Instant money transfers and payment settlements.

- Reduced Operational Costs: Automation cuts manual processing costs.

- Faster Loan Approvals: AI streamlines underwriting processes.

- Centralized Data Management: Unified platforms for better resource utilization.

C. Data-Driven Decision-Making

- Predictive Analytics: Forecasting customer needs and trends.

- Risk Assessment Models: AI-based risk profiling for better loan management.

- Churn Prediction: Identifying at-risk customers and retaining them.

- Fraud Detection: Real-time identification of suspicious activities.

- Market Analysis: Insights for targeted product launches.

D. Financial Inclusion

- Access to Remote Areas: Digital banking reaches underbanked regions.

- Microloans: AI-driven credit assessments for small-scale borrowers.

- Digital Wallets: Simplified transactions for unbanked populations.

- E-Learning Platforms: Educating underserved communities about financial literacy.

- Crowdfunding Initiatives: Blockchain-backed platforms for collective funding.

E. Security and Fraud Prevention

- Biometric Authentication: Fingerprint and facial recognition for secure access.

- Blockchain-Based Transactions: Immutable records prevent fraud.

- AI-Powered Cybersecurity: Detecting and mitigating threats proactively.

- Encryption Protocols: Protecting sensitive customer data.

- Tokenized Transactions: Enhanced security for digital payments.

F. Cost Optimization

- Eliminating Physical Branches: Focus on digital-only banking services.

- Shared Services: Open banking platforms for resource sharing.

- Energy-Efficient Data Centers: Sustainable digital infrastructure.

- Reduced Compliance Costs: Automated regulatory reporting.

- Lower Marketing Expenses: Digital advertising powered by analytics.

G. Emerging Technologies in Banking

- Blockchain for Transparency: Smart contracts for automated processes.

- Internet of Things (IoT): Wearable banking devices for convenience.

- Quantum Computing: Advanced risk modeling and encryption.

- Cloud Computing: Scalable storage and services.

- 5G Integration: Faster mobile banking services.

H. New Revenue Streams

- Embedded Finance: Integrating financial services into non-banking apps.

- Open Banking APIs: Partnerships with fintechs for new products.

- Digital Wealth Management: Robo-advisors for investments.

- Tokenized Assets: Blockchain-enabled trading of real estate and securities.

- Subscriptions: Premium banking services for tailored benefits.

I. Customer Empowerment

- Self-Service Banking: Automated kiosks and app functionalities.

- Financial Planning Tools: AI-driven budgeting assistants.

- Credit Score Tracking: Real-time updates on credit performance.

- Gamified Savings Programs: Encouraging better financial habits.

- Transparent Loan Terms: Blockchain-enabled clarity in lending.

J. Workforce Transformation

- Upskilling Programs: Training employees in digital tools.

- Virtual Assistants for Employees: AI to improve workplace productivity.

- Decentralized Work Models: Remote working enabled by secure systems.

- Collaborative Platforms: Real-time project management.

- AI-Augmented Decision Making: Supporting executives with analytics.

K. Future of Payments

- Cryptocurrency Integration: Banks accepting digital currencies.

- Central Bank Digital Currencies (CBDCs): Bridging traditional and digital systems.

- Contactless Payments: Enhanced adoption of NFC technology.

- Cross-Border Instant Payments: Blockchain for fast global transfers.

- IoT Payments: Transactions via smart devices.

L. Customer Loyalty Programs

- Blockchain Rewards: Transparent tracking of points.

- Tailored Offers: AI-powered promotional campaigns.

- Engagement Gamification: Interactive savings goals.

- Real-Time Feedback Systems: Improving service based on instant reviews.

- Dynamic Interest Rates: Personalized rates based on loyalty.

M. Regulatory Compliance

- AI-Driven Compliance Monitoring: Reducing human error.

- Real-Time Reporting: Automated submissions to regulators.

- AML and KYC Automation: Faster, more accurate checks.

- Data Residency Compliance: Ensuring laws on data storage are met.

- Global Standardization: Blockchain ensures uniform reporting.

N. Sustainability Initiatives

- Green Loans: Incentivizing eco-friendly projects.

- Paperless Banking: Digital documents replace physical ones.

- Carbon Footprint Analytics: Helping customers track and reduce emissions.

- Sustainable Investments: ESG-focused portfolios.

- Energy-Efficient Systems: Blockchain and AI reduce resource use.

O. Competitive Advantages for Banks

- Faster Product Development: Agile, tech-driven approaches.

- Customer Retention: Engaging experiences through personalization.

- Cost Leadership: Optimized expenses from digital solutions.

- Global Reach: Digital platforms eliminate geographical barriers.

- Collaborations with Fintechs: Joint ventures for innovation.

P. Social Impact

- Accessible Banking for All: Reaching underserved demographics.

- Empowering Women Entrepreneurs: Digital microloans for startups.

- Disaster Relief Funds: Blockchain for transparent allocation.

- Support for Small Businesses: AI tools for better financial management.

- Community Development Initiatives: Funding programs using blockchain transparency.

Q. Challenges and Solutions

- Addressing Cybersecurity Risks: Investing in advanced protection.

- Bridging Digital Divides: Affordable banking apps.

- Ensuring Data Privacy: Compliance with global standards.

- Managing Technological Debt: Incremental system upgrades.

- Mitigating Bias in AI Models: Transparent algorithms.

R. Industry Evolution

- Collaborative Ecosystems: Partnerships across industries.

- Decentralized Finance (DeFi): Challenging traditional models.

- AI-Centric Banks: Fully automated operations.

- Hybrid Models: Combining traditional and digital banking.

- Next-Gen ATMs: Smart kiosks with blockchain integration.

S. Trends to Watch

- Banking in the Metaverse: Virtual customer interactions.

- Digital Twin Branches: Simulated physical banks.

- Edge Computing: Processing data closer to the source.

- Predictive AI for Market Trends.

- Tokenized Banking Products: Fractional ownership in loans.

T. Future of Banking Leadership

- AI-Driven Insights for Executives.

- Sustainability as a Core Goal.

- Open Banking Leadership: Setting standards.

- Data-First Decision Culture.

- Crisis-Ready Digital Systems.

- Customer-Centric Innovations: Continuously adapting to needs.

Benefits to Banks and Customers

For Banks:

- Higher operational efficiency and cost savings.

- Improved customer loyalty and retention.

- New revenue opportunities through digital products.

For Customers:

- Enhanced convenience and faster services.

- Access to innovative financial tools.

- Increased transparency and trust in banking.

Summary

Digital transformation is reshaping banking in 2024, offering innovative solutions for challenges and creating growth opportunities. With customer satisfaction at the core, banks leveraging technology will thrive in this competitive landscape.

Conclusion

Embracing digital transformation is no longer optional for banks — it’s a necessity. By fostering collaboration, ensuring security, and prioritizing customer experience, the banking sector can redefine its future.

Thank You

Thank you for exploring the transformative effects of digital banking in 2024. Together, we can embrace innovation for a brighter financial future!